Got deductions? TCJA and the 20% deduction for qualified business income

by Jay A. Goldman

One major component of the new federal tax law that impacts most pass-through entities – such as S Corporations and LLCs – is the 20 percent deduction for qualified business income (QBI).

Also known as Section 199A, this provision in the Tax Cuts and Jobs Act was an attempt to level the playing field for pass-throughs as a result of the new lower income tax rate for C corporations.

Currently, the highest tax rate for individuals is 37 percent. If you qualify for the full 20 percent deduction and remain in the highest tax bracket, your pass-through income tax rate is effectively reduced to 29.6 percent. This compares favorably to the 39.6 percent you likely paid last year and the 21 percent that C corporations pay when you consider the double taxation (the taxes the C Corp pays as well as taxes shareholders then pay on distributed profits).

To be eligible for the 199A deduction, you have to be in the right type of business and have certain levels of fixed assets and wages paid. In general, the 199A deduction is 20 percent of qualified business income limited to the greater of (A) 50 percent of the W-2 wages paid by the business or (B) the sum of 25 percent of the W-2 wages paid by the business, plus 2.5 percent of the unadjusted basis of tangible property owned by the business.

199A and selling your business

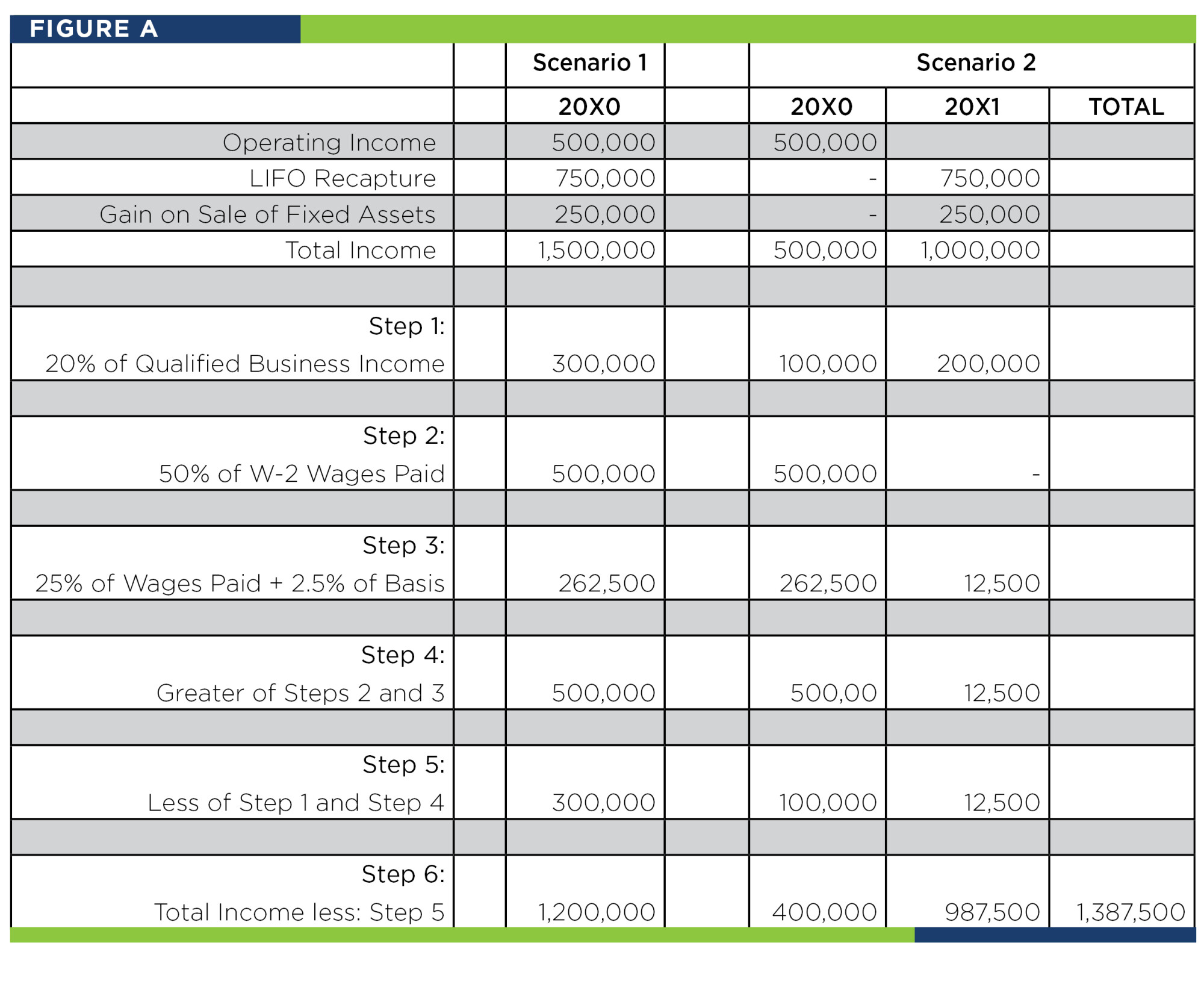

Let’s assume you have the following facts:

Net income for Year 20X0 – $500,000

LIFO Reserve at the end of Year 20X0 – $750,000

W-2 Wages Paid in 20X0 – $1,000,000

Qualified Tangible Property Owned By Business at the end of 20X0:

Original Cost of $500,000, Fully Depreciated but still within its useful life

Now, let’s assume you are going to sell your business in an asset sale and that tangible property accounts for $250,000 of the sale price. Any ordinary income resulting from the sale is eligible for the 199A deduction if the other limits are met. Any capital gain income is not.

If the sale taxes place December 31, 20X0, your taxable income (excluding any capital gain) would be $1.2 million. If the sale does not take place until January 1, 20X1, your taxable income (excluding any capital gain) would be $1,387,500. Assuming the highest individual tax bracket of 37 percent, that is an additional $69,375 in tax.

The fact that a taxpayer would have a different tax result for the same transaction depending on when in the tax year settlement occurs seems unreasonable.

The Treasury Department was made aware of this phenomenon during the current comment period on the proposed regulations. It’s hoped the department will offer some form of a workaround – including perhaps a look-back period to wages paid in the prior year – or something similar – when selling a business.

Jay A. Goldman, CPA, is a principal with Boyer & Ritter LLC. His primary responsibilities include servicing the accounting, tax and consulting needs of the firm’s auto dealership clients. Contact Jay at 717-761-7210 or jgoldman@cpabr.com