3 tips for ensuring your school district's single audit goes smoothly

by Cathy L. Harlow

by Cathy L. Harlow

While school districts routinely receive federal funding, additional COVID-19 grants may require something new: a single audit showing grant compliance.

If your district expended $750,000 or more over the past fiscal year in federal funding you are required to obtain a single audit. This includes federal funds which were received either directly or indirectly from a pass-through entity as a subrecipient.

The following are key steps to ensure an accurate single audit:

1. Gather information about your grants.

Once you determine that you hit the single audit threshold, gather the information about the grants your district received. This should include award documentation, the grant’s Catalog of Federal Domestic Assistance (CFDA) number, general ledger detail, and reports submitted for the grant.

Grant CFDA numbers are generally available on the Pennsylvania Department of Education audit confirmation, available through the Financial Accounting Information System (FAI). They are also typically included on the grant application.

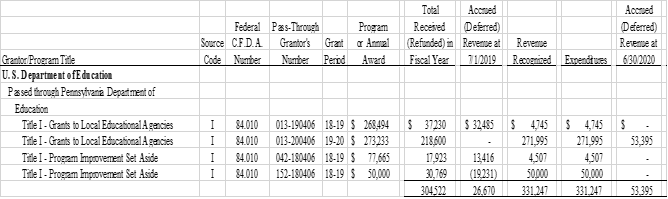

After you have gathered all the grant documentation and CFDA number you will need to prepare a schedule of expenditures and federal awards. Below is an example of the Schedule and detailed information on how to prepare it.

- Column 1: Identify the federal grantor agency as well as the pass-through agency. Then list each grant separately. Do not combine grants with the same title or CFDA number.

- Column 2: Indicate if the grant came directly from the federal government or indirectly through another agency. Most federal grants come indirectly through the Pennsylvania Department of Education or another entity such as the Intermediate Unit.

- Column 3: The grant’s CFDA number.

- Column 4: Determine the pass-through grantor’s number from the grant application. Indicate NA if there is not one.

- Columns 5 and 6: Check your grant application for the funding period and award amount. Often the grant award amount for Title programs may change during the year, so be sure to document the revised amounts and include them on the schedule.

- Column 7: You can obtain the amount received or refunded from the PDE Audit confirmation or by reviewing your general ledger detail.

- Column 8: The amount of Accrued or Deferred Revenue as of July 1, XXX should be obtained from your audit report from the prior year, which would include the previous year’s SEFA. If this is the first year that a single audit is required, you should be able to obtain the amount that was accrued or deferred for each grant from your listing of federal accounts receivable or deferred revenue from the prior year. If necessary, contact your auditors to request this information.

- Columns 9 and 10: These columns will typically be the same. The amount is determined by the total funds expended during the fiscal year for the program and should match the general ledger detail for each grant.

- Column 11: Calculate the accrual of deferral for the end of the fiscal year by taking the beginning accrual (deferral), subtracting the amount received during the year, and subtracting the amount expended.

Note: The SEFA should include subtotals for each CFDA number as well as the total amount of federal awards received and expended.

2. Ensure your district followed grant guidelines

Make sure your district follow’s the requirements as outlined in the Office of Management and Budget (OMB) issued “Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards”, commonly referred to as the Uniform Guidance. You should have the required policies in place and follow the required procedures especially related to allowability of costs and procurement.

In addition, your financial records should show how your expenditures were in line with the grant’s guidelines.

We advise keeping grants in separate accounts so expenditures – and guideline compliance – is easy to track.

3. Double-check your compliance

Did you use more than one grant for the same purpose by mistake? Do your expenditure reports match actual grant spending? Review your district’s internal controls over compliance – which are part of the audit – to ensure transactions are properly recorded and accounted for.

Common mistakes and pitfalls

- Incorrectly reporting expenditures: Districts must submit quarterly reports showing grant expenditures. Some districts find that the quarterly reports fail to agree with the actual amount spent or do not mesh with their general ledger. In one case, the person preparing the quarterly reports kept manual records of the amount of funds spent which did not agree to the general ledger, resulting in inaccurate reporting of expenditures.

- Failing to correctly identify funding sources: Ensure you have the correct CFDA numbers and accurately identify the funding sources – both the federal awarding agency and the pass-through entity. At times, districts fail to realize a grant source is federal and subject to the audit. When in doubt, check with the grantor.

- Lack of communication: Your grants manager needs to communicate with your business manager frequently. At a minimum, they should meet quarterly to ensure grant requirements are being followed, funds are being spent in accordance with the grant guidelines, and that the transactions are being recorded correctly in the general ledger.

Bottom line

Preparing a single audit is complex, and the requirements can be confusing, especially for districts doing it for the first time. However, the expert team at Boyer & Ritter is ready to help with any questions or problems to ensure an accurate and headache-free process.